Alright, let’s cut the crap.

The champagne corks are popping over at Tesla, and every finance bro with a Robinhood account is taking a victory lap because the Q3 delivery numbers are in. Nearly half a million cars. The `tsla stock price` shot past $444 like a SpaceX rocket. On the surface, it’s a beautiful, shiny picture of success.

But I’ve been doing this long enough to know that when a company shines a spotlight this bright on one number, it’s usually because they’re trying to keep you from looking at the dark, ugly thing hiding in the corner. And boy, is there an ugly thing.

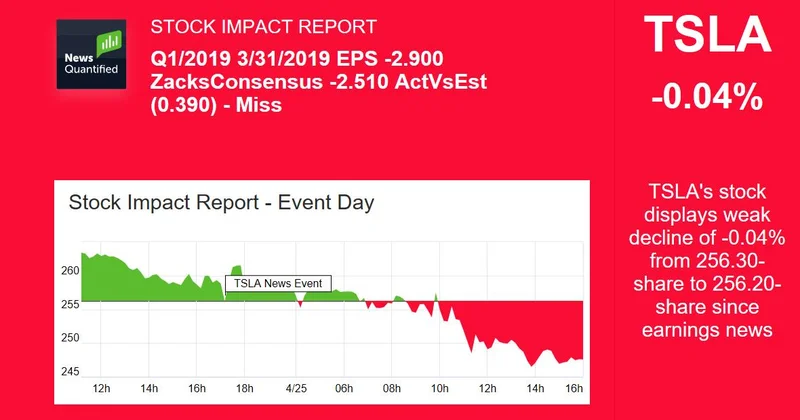

While everyone's high-fiving over deliveries, the earnings per share—you know, the actual profit—is projected to have cratered by 24%. Let that sink in. They’re selling more cars than ever and somehow making dramatically less money on each one. This isn't a victory lap; it's the financial equivalent of running in place while convincing yourself you're winning a marathon.

So, what gives? How can a company be soaring and sinking at the same time? And why is nobody else asking this question?

The Volume-Over-Value Shell Game

Let’s be real. The only reason Tesla is hitting these massive delivery numbers is because they’ve been slashing prices all year. They’re chasing market share with the desperation of a middle-aged man buying a sports car. The automotive gross margin, once the envy of the industry at over 25%, is now sputtering around 18%. That’s a hell of a drop.

This is the classic volume-over-value trap. It’s like a hot dog vendor who decides to become the biggest name in the city by selling his hot dogs for a dime. Sure, the line is around the block and the sales charts look incredible, but at the end of the day, he's going broke one hot dog at a time. Is that really a sustainable business model, or just a way to keep the stock price inflated?

The market’s reaction is what truly baffles me. The `tsla stock` doubles in six months while the core profitability of its main product is actively eroding. This is a bad sign. No, "bad" doesn't cover it—this is a five-alarm fire in the engine block that everyone is pretending is just a neat new hood ornament.

The institutional investors—BlackRock, Vanguard, all the usual suspects—are still holding on for dear life. Are they seeing something I’m not, or are they just too big to admit they might have backed the wrong horse? The whole thing feels less like a sound investment strategy and more like a collective faith-based initiative. Meanwhile, the competition from companies like BYD ain't sleeping. They're not just catching up; in many markets, they're already pulling ahead, and they built their empires on affordable, mass-market EVs from the start. Tesla is playing catch-up in a game it thought it had already won.

Selling a Future That Never Quite Arrives

Whenever you point out the cracks in today's foundation, the Tesla faithful immediately pivot to the glorious, world-changing promises of tomorrow. It's always about the next thing.

First, it was the 4680 battery cells, the magic beans that were supposed to cut production costs by 50%. We’ve been hearing about those for years, and while they're slowly making their way into cars, they haven't exactly revolutionized the balance sheet, have they? Then there's the long-promised "Model 2," the mythical sub-$27,000 compact car supposedly coming in late 2026. How, exactly, do you plan to make a profit on a $27,000 car when your margins on $40,000 cars are already in the toilet? The math just doesn't work unless there's some technological miracle they're hiding in a lab somewhere.

And offcourse, the ultimate get-out-of-jail-free card: the Robotaxi. The "CyberCab." A future where no one owns cars and we're all just passengers in Elon's autonomous utopia. I can almost hear the investor call now. Some brave soul asks about the declining margins, and the response is a 20-minute sermon on how Tesla isn't even a car company, it's an AI robotics company. It's brilliant, in a deeply cynical way. You don't have to answer for this quarter's failures if you can get everyone to dream about 2030's fortunes.

I see this pattern across the tech world. The `nvda stock price` isn't just about the chips they sell today; it's about a belief in an AI-dominated future. Same with `amd stock`. But with Tesla, it feels... different. More fragile. The promises are so grand, so reality-altering, that they create a force field against any criticism of the here and now. They point to the sky, and everyone looks up, and I just... I can't help but stare at the P&L statement and wonder if I'm the only one who sees the disconnect.

A Sugar High That's Bound to Crash

Look, I'm not saying Tesla is going to implode tomorrow. They're still moving a ton of metal and their energy storage business is legitimately impressive, hitting a record 12.5 GWh this quarter. That’s a real, tangible success.

But the valuation of the company, the breathless coverage, the cult-like devotion to the `tsla stock price today`—it's all based on the idea that Tesla Rides High Before Q3 Earnings With (TSLA) Stock Rising, Record Deliveries, Gigafactory Growth, and Green Goals is a revolutionary tech company with untouchable margins. The Q3 numbers prove that, at its core, it's becoming just another car company. And car companies are judged on boring things like production efficiency, supply chains, and, yes, profit margins.

The market is currently treating Tesla like it's immune to gravity. But gravity always, always wins. The sugar high from these delivery numbers will wear off, and what's left will be a company facing fierce competition, shrinking profits, and a slate of futuristic promises that are still years away from paying the bills. And you have to wonder how long investors will keep buying the dream when the reality is getting harder and harder to ignore.